CB

UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM CB

TENDER OFFER/RIGHTS OFFERING NOTIFICATION FORM

Please place an X in the box(es) to designate the appropriate rule provision(s) relied upon to file this Form:

|

|

|

|

|

|

|

| Securities Act Rule 801 (Rights Offering) |

|

¨ |

|

|

|

|

| Securities Act Rule 802 (Exchange Offer) |

|

x |

|

|

|

|

| Exchange Act Rule 13e-4(h)(8) (Issuer Tender Offer) |

|

¨ |

|

|

|

|

| Exchange Act Rule 14d-1(c) (Third Party Tender Offer) |

|

x |

|

|

|

|

| Exchange Act Rule 14e-2(d) (Subject Company Response) |

|

¨ |

|

|

|

|

|

|

|

| Filed or submitted in paper if permitted by Regulation S-T Rule 101(b)(8) |

|

¨ |

|

|

|

|

Meda AB

(Name of

Subject Company)

Not applicable

(Translation of Subject Company’s Name into English (if applicable)

Sweden

(Jurisdiction of

Subject Company’s Incorporation or Organization)

Mylan N.V.

(Name of Person(s) Furnishing Form)

Shares

(Title of Class

of Subject Securities)

Not Applicable

(CUSIP Number of Class of Securities (if applicable))

Dr. Jörg-Thomas Dierks, CEO

Box 906

SE-170 09 Solna,

Sweden

Telephone: +46 8 630 19 00

(Name, Address (including zip code) and Telephone Number (including area code) of

Person(s) Authorized to Receive Notices and Communications on Behalf of Subject Company)

Copies to:

Joseph F. Haggerty

Corporate Secretary

Mylan

N.V.

c/o Mylan Inc.

1000 Mylan Boulevard

Canonsburg, Pennsylvania 15317

Tel: (724) 514-1800

and

|

|

|

| Bradley L. Wideman, Esq.

Vice President, Associate General Counsel,

Securities and Assistant Secretary

Mylan N.V. c/o Mylan

Inc. 1000 Mylan Boulevard

Canonsburg, Pennsylvania 15317

(724) 514-1800 |

|

Mark I. Greene, Esq.

Thomas E. Dunn, Esq. Aaron

M. Gruber, Esq. Cravath, Swaine & Moore LLP

825 Eighth Avenue New York,

New York 10019 (212) 474-1000 |

June 17, 2016

(Date Tender Offer/Rights Offering Commenced)

PART I – INFORMATION SENT TO SECURITY HOLDERS

Item 1. Home Jurisdiction Documents

|

|

|

| Exhibit No. |

|

Description |

|

|

| 99.1 |

|

English Translation of Swedish Offer Document, published on June 16, 2016. |

| 99.2 |

|

EU Prospectus, published on June 16, 2016. |

(b) Not applicable.

Item 2. Informational Legends

The below

legend was mailed along with the Swedish Offer Document to the Meda AB shareholders and has been included on a webpage required to be clicked through prior to accessing the Swedish Offer Document, which has been published on Mylan N.V.’s

website, medatransaction.mylan.com, in accordance with Swedish requirements:

“Special notice to shareholders in the United States

This Offer is made for the securities of a foreign company. The Offer is subject to disclosure requirements of a foreign country that are different from those

of the United States. Certain financial statements included or incorporated by reference in the document, have been prepared in accordance with foreign accounting standards that may not be comparable to the financial statements of U.S. companies.

It may be difficult for investors to enforce their rights and any claim they may have arising under the federal securities laws, since Meda is

incorporated in Sweden and Mylan is incorporated in the Netherlands, and some or all of their respective officers and directors may be residents of a foreign country. Investors may not be able to sue a foreign company or its officers or directors in

a foreign court for violations of the U.S. securities laws. It may be difficult to compel a foreign company and its affiliates to subject themselves to a U.S. court’s judgment.

Investors should be aware that Mylan may purchase securities otherwise than under the Offer, such as in open market or privately negotiated purchases.”

PART II – INFORMATION NOT REQUIRED TO BE SENT TO SECURITY HOLDERS

PART III – CONSENT TO SERVICE OF PROCESS

PART IV – SIGNATURES

After due inquiry and to the best of my knowledge and belief, I certify that the information set forth in this statement is true, complete and correct.

|

|

|

| MYLAN N.V. |

|

|

| By: |

|

/s/ Kenneth S. Parks |

| Name: |

|

Kenneth S. Parks |

| Title: |

|

Chief Financial Officer |

Date: June 17, 2016

EX-99.1

Exhibit 99.1

Mylan’s offer to the

shareholders of Meda

Important information

This offer document (this “Offer Document”) has been prepared in accordance with the Swedish Financial Instruments Trading Act

(SFS 1991:980) (the “Trading Act”), the Swedish Takeover Act (Sw. lagen om offentliga uppköpserbjudanden på aktiemarknaden) (the “Takeover Act”) and Nasdaq Stockholm’s Takeover Rules (the

“Takeover Rules”). This Offer Document has been prepared in Swedish and English. In the event of any discrepancy in content between the language versions, the Swedish version shall prevail.

The Swedish version of this Offer Document has been approved and registered by the Swedish Financial Supervisory

Authority (Sw: Finans inspektionen) (the “SFSA”) pursuant to the provisions of Chapter 2 of the Takeover Act and Chapter 2a of the Trading Act. Approval and registration by the SFSA do not imply that the SFSA

guarantees that the information provided in this Offer Document is correct or complete.

Mylan N.V.’s

(“Mylan”) public offer to the shareholders of Meda Aktiebolag (publ.) (“Meda”) in accordance with the terms specified in this Offer Document (the “Offer”) and this Offer Document are governed by and construed in all

respects in accordance with the substantive laws of Sweden, without regard to any conflict of law principles leading to the application of laws of any other jurisdiction. The Takeover Rules and the Swedish Securities Council’s rulings and

statements on the application and interpretation of the Takeover Rules apply to the Offer. In accordance with the Takeover Act, Mylan has contractually undertaken towards Nasdaq Stockholm to comply with the rules established by Nasdaq Stockholm for

such offers and submit to any sanctions that Nasdaq Stockholm can impose on Mylan in the event of a breach of the Takeover Rules. On February 10, 2016, Mylan informed the SFSA about the commitment to Nasdaq Stockholm. Any dispute regarding the

Offer, or which arises in connection with the Offer or this Offer Document, shall be settled exclusively by Swedish Courts, and the City Court of Stockholm shall be the court of first instance.

The information in this Offer Document is only provided in contemplation of the Offer and may not be used for any other

purpose. There is no guarantee that the information provided in this Offer Document is current as of any date other than the date of the publication of this Offer Document or that there have not been any changes in Mylan’s or Meda’s

business since that date. If the information in this Offer Document becomes subject to any material change, such material change will be made public in accordance with the provisions of the Trading Act, which governs the publication of supplements

to this Offer Document.

Except for what is stated on pages 97, 130 and 184, or otherwise expressly stated in this

Offer Document, no information in this Offer Document has been reviewed by Mylan’s auditors or reporting accountants or Meda’s auditors. The figures reported in this Offer Document have in some cases been rounded off, and as a result the

figures in tables may not tally with the stated totals.

Additional information

In connection with the Offer, Mylan has filed certain materials with the Securities and Exchange Commission (the “SEC”),

including, among other materials, a Registration Statement on Form S-4 filed on April 11, 2016 (as amended on May 13, June 3 and June 14, 2016, the “Registration Statement”). Mylan has also filed the prospectus to be issued in

connection with the Offer (the “EU Prospectus”) with the Netherlands Authority for the Financial Markets (Autoriteit Financiële Markten) (the “AFM”), which will published upon approval by the AFM. This Offer Document

is not intended to be, and is not, a substitute for such documents or for any other document that Mylan may file with the SEC, the AFM or any other competent EU authority in connection with the Offer. This Offer Document contains advertising

materials (reclame-uitingen) in connection with the Offer as referred to in Section 5:20 of the Dutch Financial Supervision Act (Wet op het financieel toezicht). INVESTORS AND SECURITYHOLDERS OF MEDA IN SWEDEN AND INVESTORS AND

SECURITYHOLDERS OF MEDA IN THE EUROPEAN ECONOMIC AREA BUT OUTSIDE OF SWEDEN ARE URGED TO READ THE OFFER DOCUMENT THAT IS APPROVED BY THE SFSA AND ANY SUPPLEMENT THERETO, OR THE EU PROSPECTUS THAT IS APPROVED BY THE AFM AND ANY SUPPLEMENT THERETO, AS

APPLICABLE, CAREFULLY AND IN THEIR ENTIRETY BEFORE MAKING AN INVESTMENT DECISION BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT MYLAN, MEDA AND THE OFFER. INVESTORS AND SECURITYHOLDERS OF MEDA OUTSIDE THE EUROPEAN ECONOMIC AREA ARE URGED TO

READ ANY DOCUMENTS FILED WITH THE SFSA, THE SEC AND THE AFM OR ANY OTHER COMPETENT EU AUTHORITY CAREFULLY AND IN THEIR ENTIRETY (IF AND WHEN THEY BECOME AVAILABLE) BEFORE MAKING AN INVESTMENT DECISION BECAUSE THEY WILL EACH CONTAIN IMPORTANT

INFORMATION ABOUT MYLAN, MEDA AND THE OFFER. Such documents are or upon publication will be available free of charge through the website maintained by the SEC at www.sec.gov, on Mylan’s website at medatransaction.mylan.com or, to the extent

filed with the AFM, through the website maintained by the AFM at www.afm.nl, or by directing a request to Mylan at +1 (724) 514-1813 or investor.relations@mylan.com. Any materials filed by Mylan with the SFSA, the SEC, the AFM or any other competent

EU authority that are required to be mailed to Meda shareholders will also be mailed to such shareholders. A copy of this Offer Document will be available free of charge at the following website: medatransaction.mylan.com.

Further information

The Offer, pursuant to the terms and conditions presented in Mylan’s offer announcement dated February 10, 2016 and in this Offer

Document, is not being made to persons whose participation in the Offer requires that an additional offer document or prospectus be prepared or registration effected or that any other measures be taken in addition to those required under Swedish law

(including the Takeover Rules), Dutch law, Danish law, Irish law, United Kingdom law and U.S. law.

The distribution

of this Offer Document and any related Offer documentation in certain jurisdictions may be restricted or affected by the laws of such jurisdictions. Accordingly, copies of this Offer Document are not being, and must not be, mailed or otherwise

forwarded, distributed or sent in, into or from any such jurisdiction. Therefore, persons who receive this Offer Document (including, without limitation, nominees, trustees and custodians) and are subject to the laws of any such jurisdiction

will need to inform themselves about, and observe, any applicable restrictions or requirements. Any failure to do so may constitute a violation of the securities laws of any such jurisdiction. To the fullest extent permitted by applicable

law, Mylan disclaims any responsibility or liability for the violations of any such restrictions by any person.

The

Offer is not being made, and this Offer Document may not be distributed, directly or indirectly, in or into, nor will any tender of shares be accepted from or on behalf of holders in, Australia, Hong Kong, Japan, Canada, New Zealand or South

Africa, or any other jurisdiction in which the making of the Offer, the distribution of this Offer Document or the acceptance of any tender of shares would contravene applicable laws or regulations or require further offer documents, filings or

other measures in addition to those required under Swedish law (including the Takeover Rules), Dutch law, United Kingdom law, Danish law, Irish law and U.S. law.

With regard to Meda shareholders in the European Economic Area but outside Sweden, any election to accept the Offer

should only be made on the basis of information contained in the EU Prospectus that is approved by the AFM and any supplement thereto. In addition, Meda shareholders outside the European Economic Area should consider the information contained in the

Registration Statement that is declared effective by the SEC. It may be unlawful to distribute the EU Prospectus or this Offer Document in certain jurisdictions. The AFM will be requested to provide the Danish Financial Supervision Authority

(“DFSA”), the Central Bank of Ireland (“CBI”) and the UK Financial Conduct Authority (“FCA”), with a certificate of approval attesting that the EU Prospectus has been drawn up in accordance with Directive 2003/71/EC of

the European Parliament and of the Council of 4 November 2003, as amended.

Forward-looking information

This Offer Document contains “forward-looking statements.” Such forward-looking statements may include, without limitation,

statements about Mylan’s proposed transaction to acquire Meda (the “Transaction”), the Offer, Mylan’s acquisition (the “EPD Transaction”) of Mylan Inc. and Abbott Laboratories’ non-U.S. developed markets specialty

and branded generics business (the “EPD Business”), the benefits and synergies of the EPD Transaction and the Transaction, future opportunities for Mylan, Meda, or the combination of Mylan and Meda if the Offer is completed (the

“Combined Company”) and products and any other statements regarding Mylan’s, Meda’s or the Combined Company’s future operations, anticipated business levels, future earnings, planned activities, anticipated growth, market

opportunities, strategies, competition, and other expectations and targets for future periods. These may often be identified by the use of words such as “will,” “may,” “could,” “should,” “would,”

“project,” “believe,” “anticipate,” “expect,” “plan,” “estimate,” “forecast,” “potential,” “intend,” “continue,” “target” and variations of

these words or comparable words. Because forward-looking statements inherently involve risks and uncertainties, actual future results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause

or contribute to such differences include, but are not limited to: uncertainties related to the Transaction, including as to the timing of the Transaction, uncertainties as to whether Mylan will be able to complete the Transaction, the possibility

that competing offers will be made, the possibility that certain conditions to the completion of the Offer will not be satisfied, and the possibility that Mylan will be unable to obtain regulatory approvals for the Transaction or be required, as a

condition to obtaining regulatory approvals, to accept conditions that could reduce the anticipated benefits of the Transaction; the ability to meet expectations regarding the accounting and tax treatments of the Transaction and the EPD Transaction,

changes in relevant tax and other laws, including but not limited to changes in the U.S. tax code and healthcare and pharmaceutical laws and regulations in the U.S. and abroad; the integration of the EPD Business and Meda being more difficult,

time-consuming, or costly than expected; operating costs, customer loss and business disruption (including, without limitation, difficulties in maintaining relationships with employees, customers, clients, or suppliers) being greater than expected

following the EPD Transaction and the Transaction; the retention of certain key employees of the EPD Business and Meda being difficult; the possibility that Mylan may be unable to achieve expected synergies and operating efficiencies in connection

with the EPD Transaction and the Transaction within the expected time-frames or at all and to successfully integrate the EPD Business and Meda; expected or targeted future financial and operating performance and results; the capacity to bring new

products to market, including but not limited to where Mylan uses its business judgment and decides to manufacture, market, and/or sell products, directly or through third parties, notwithstanding the fact that allegations of patent infringement(s)

have not been finally resolved by the courts (i.e., an “at-risk launch”); any regulatory, legal, or other impediments to Mylan’s ability to bring new products to market; success of clinical trials and Mylan’s ability to execute

on new product opportunities; any changes in or difficulties with Mylan’s inventory of, and its ability to manufacture and distribute, the EpiPen® Auto-Injector to meet anticipated

demand; the scope, timing and outcome of any ongoing legal proceedings and the impact of any such proceedings on financial condition, results of operations and/or cash flows; the ability to protect intellectual property and preserve intellectual

property rights; the effect of any changes in customer and supplier relationships and customer purchasing patterns; the ability to attract and retain key personnel; changes in third-party relationships; the impact of competition; changes in the

economic and financial conditions of the businesses of Mylan, Meda or the Combined Company; the inherent challenges, risks, and costs in identifying, acquiring, and integrating complementary or strategic acquisitions of other companies, products or

assets and in achieving anticipated synergies; uncertainties and matters beyond the control of management; and inherent uncertainties involved in the estimates and judgments used in the preparation of financial statements, and the providing of

estimates of financial measures, in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), International Financial Reporting Standards (“IFRS”) and related standards or on an

adjusted basis. For more detailed information on the risks and uncertainties associated with Mylan’s business activities, see the risks described in Mylan’s Annual Report on Form 10-K for the year ended December 31, 2015, its Quarterly

Report on Form 10-Q for the quarterly period ended March 31, 2016 and its other filings with the SEC. These risks and uncertainties also include those risks and uncertainties that will be discussed in this Offer Document, the Registration Statement

filed with the SEC, and the EU Prospectus filed with the AFM. You can access Mylan’s filings with the SEC through the SEC website at www.sec.gov, and Mylan strongly encourages you to do so. Mylan undertakes no obligation to update any

statements herein for revisions or changes after the publication date of this Offer Document, except as required by law.

Non-GAAP and Non-IFRS financial measures

This Offer Document contains non-GAAP and non-IFRS financial measures. Non-GAAP and non-IFRS financial measures should be considered only

as a supplement to, and not as a substitute for or as a superior measure to, financial measures prepared in accordance with U.S. GAAP or IFRS, as applicable. For more information regarding such non-GAAP and non-IFRS financial measures, including

reconciliations of certain non-GAAP financial measures to their most directly comparable U.S. GAAP measure, see Appendix I to this Offer Document.

Presentation of financial and other information

This Offer Document contains historical financial

information regarding Mylan and Meda that has been derived from their respective public filings and reports. Historical financial information regarding Mylan as of and for the years ended December 31, 2015, 2014 and 2013 has been derived from

Mylan’s Annual Reports on Form 10-K for the years ended December 31, 2015, 2014 and 2013 and historical financial information regarding Mylan as of and for the three months ended March 31, 2016 and 2015 has been derived from Mylan’s

Quarterly Report on Form 10-Q for the three months ended March 31, 2016. Mylan’s consolidated financial statements and the related notes included in such Annual Reports on Form 10-K are audited, but financial information derived from other

sections of such Annual Reports on Form 10-K is unaudited. All financial information derived from Mylan’s Quarterly Report on Form 10-Q is unaudited. Historical financial information regarding Meda

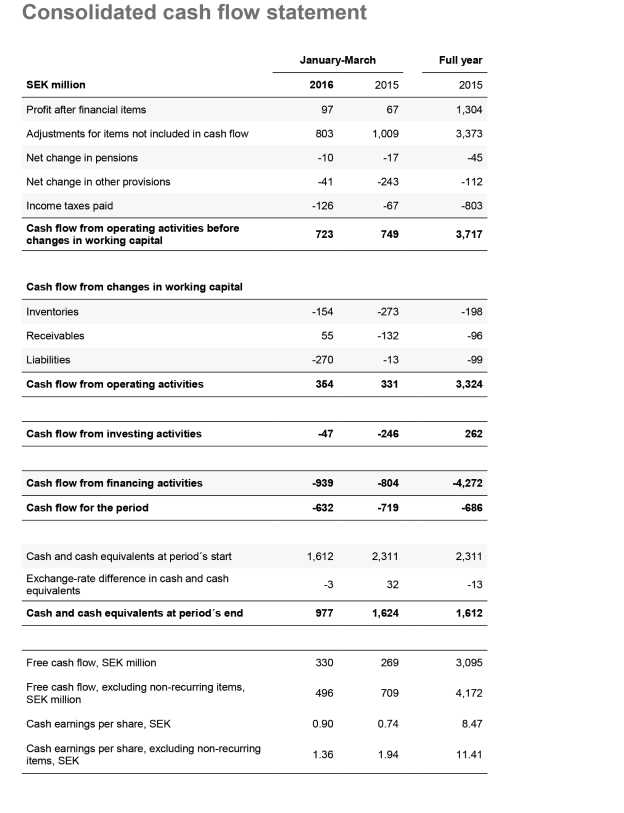

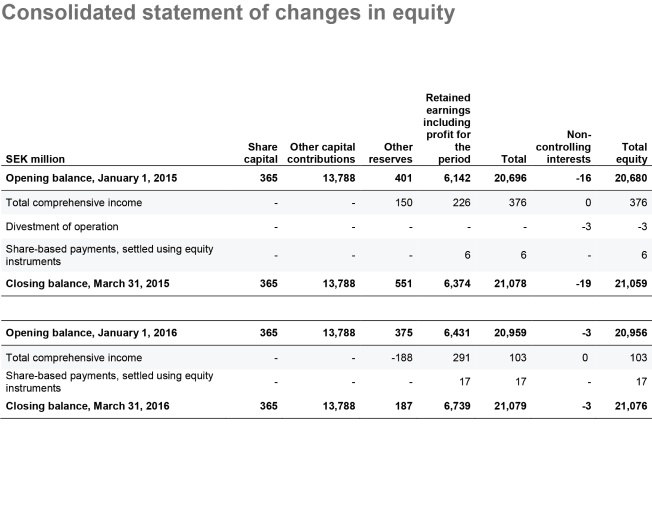

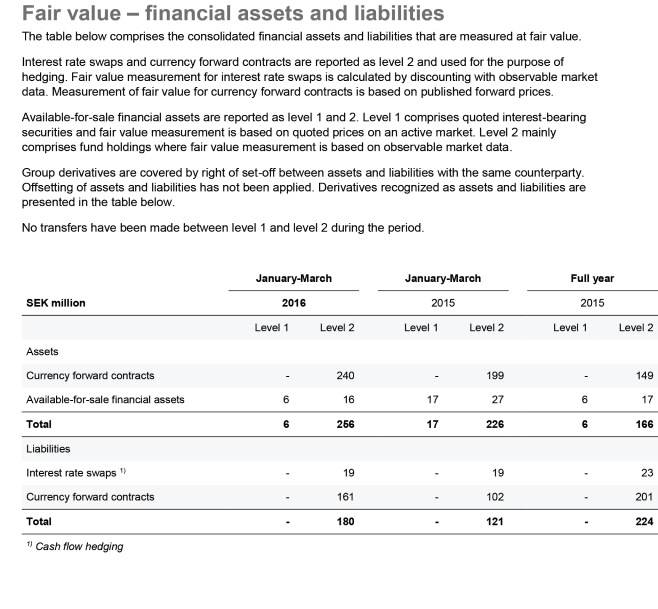

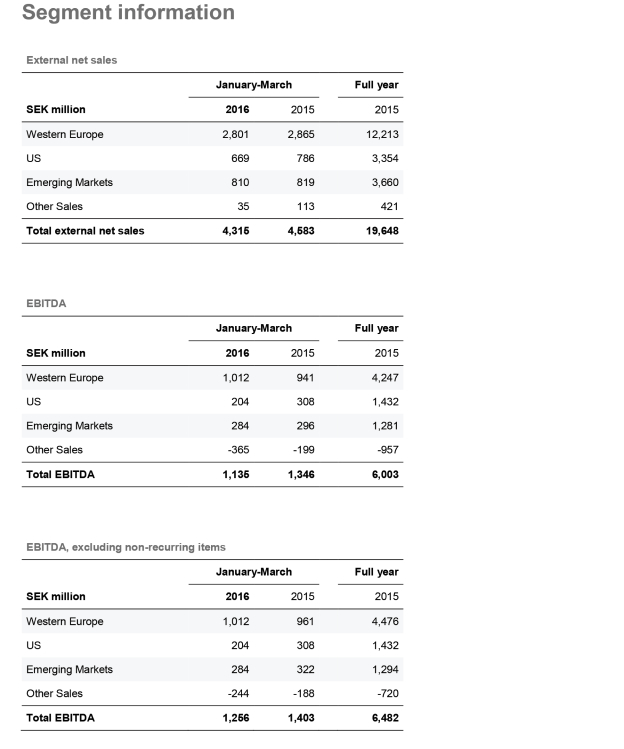

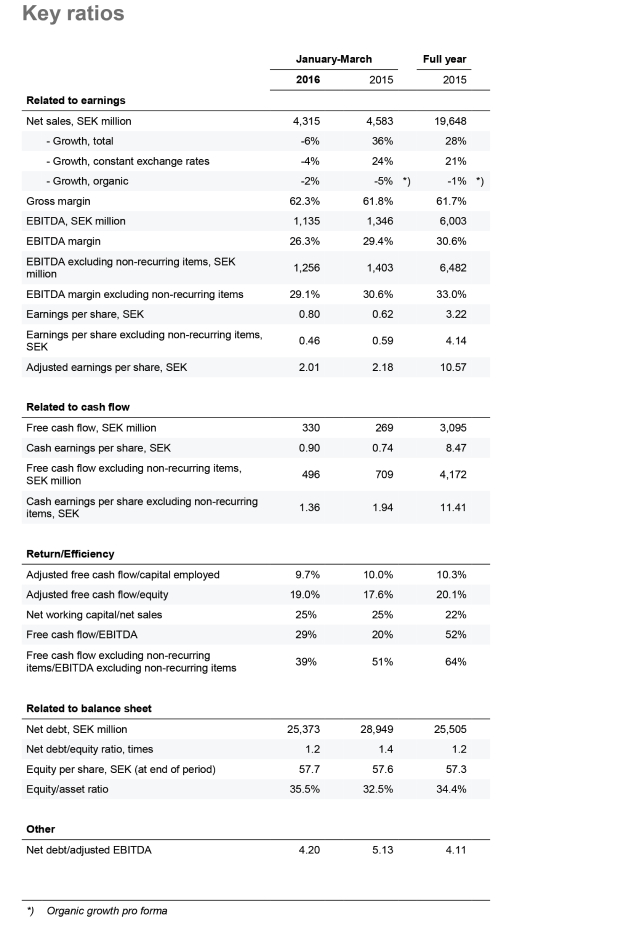

as of and for the years ended December 31, 2015, 2014 and 2013 has been derived from Meda’s Annual Reports for 2015, 2014 and 2013 and historical financial information regarding Meda as of and for the three months ended March 31, 2016 and 2015

has been derived from Meda’s Interim Report for January-March 2016.

Special notice to

shareholders in the United States

This Offer is made for the securities of a foreign

company. The Offer is subject to disclosure requirements of a foreign country that are different from those of the United States. Certain financial statements included or incorporated by reference in the document, have been prepared in accordance

with foreign accounting standards that may not be comparable to the financial statements of U.S. companies.

It

may be difficult for investors to enforce their rights and any claim they may have arising under the federal securities laws, since Meda is incorporated in Sweden and Mylan is incorporated in the Netherlands, and some or all of their respective

officers and directors may be residents of a foreign country. Investors may not be able to sue a foreign company or its officers or directors in a foreign court for violations of the U.S. securities laws. It may be difficult to compel a foreign

company and its affiliates to subject themselves to a U.S. court’s judgment.

Investors should be aware that

Mylan may purchase securities otherwise than under the Offer, such as in open market or privately negotiated purchases.

The Offer in brief

Mylan is making a recommended public offer to the shareholders of Meda to tender all their shares of Meda for the following Offer

consideration (the “Offer Consideration”):

| |

• |

|

in respect of 80 percent of the number of Meda shares tendered by each Meda shareholder, SEK 165 in cash per Meda share; and |

|

| |

• |

|

in respect of the remaining 20 percent of the number of Meda shares tendered by each Meda shareholder: |

|

| |

• |

|

(i) if the volume-weighted average sale price per Mylan ordinary share (“Mylan Share”) on the NASDAQ Global Select Stock Market (“NASDAQ”) for the 20 consecutive trading days ending on

and including the second trading day prior to the Offer being declared unconditional (the “Offeror Average Closing Price”) is greater than USD 50.74, a number of Mylan Shares per Meda share equal to SEK 165 divided by the Offeror

Average Closing Price as converted from USD to SEK at a SEK/USD exchange rate of 8.4158 (the “Announcement Exchange Rate”); |

|

| |

• |

|

(ii) if the Offeror Average Closing Price is greater than USD 30.78 and less than or equal to USD 50.74, 0.386 Mylan Shares per Meda share; or |

| |

• |

|

(iii) if the Offeror Average Closing Price is less than or equal to USD 30.78, a number of Mylan Shares per Meda share equal to SEK 100 divided by the Offeror Average Closing Price as converted from USD to SEK at the

Announcement Exchange Rate. |

| |

• |

|

If the aggregate number of Mylan Shares that otherwise would be required to be issued by Mylan as described above exceeds 28,214,081 Mylan Shares (the “Share Cap”)1, then Mylan will have the option (in its sole discretion) to (a) issue Mylan Shares in connection with the Offer in excess of the Share Cap and thus pay the share portion of the Offer

Consideration as described above (i.e. the 20 percent set out above), (b) increase the cash portion of the Offer Consideration (so that it becomes larger than the 80 percent set out above) and thus correspondingly decrease the share portion of the

Offer Consideration (so that it becomes smaller than the 20 percent set out above) such that the aggregate number of Mylan Shares issuable by Mylan in connection with the Offer would equal the Share Cap or (c) execute a combination of the

foregoing. |

|

The acceptance period for the Offer runs from and including June 17, 2016 up to and including

July 29, 2016. Settlement is expected to commence around August 10, 2016. Mylan reserves the right to extend the acceptance period and, to the extent necessary and permissible, will do so in order for the acceptance period to cover

applicable decision-making procedures at relevant authorities. Mylan also reserves the right to postpone the settlement date. For further information regarding the Offer, see “The Offer” and “Terms, conditions and

instructions.”

Mylan is making the Offer for several strategic reasons. Among others, the combination of Mylan and Meda

will create a global pharmaceutical leader that is even more diversified and has a more expansive portfolio of branded and generic medicines and a stronger and growing portfolio of over-the-counter (“OTC”) products.2 The Combined Company will have a balanced global footprint with significant scale in key geographic markets, particularly the U.S. and Europe. The acquisition of Meda also provides Mylan with entry

into a number of new and attractive emerging markets, including China, Southeast Asia, Russia, the Middle East and Mexico, complemented by Mylan’s presence in India, Brazil and Africa. Mylan and Meda have a highly complementary therapeutic

presence, which will create a leading global player in respiratory / allergy, and achieve critical mass in dermatology and pain, offering greater opportunities for growth in these categories.3

The Offer provides immediate and significant value to Meda shareholders and is supported by the Meda Board of

Directors (the “Meda Board”) and Meda’s two largest shareholders, representing approximately 30 percent of Meda’s outstanding shares. If the Offer is completed, Meda shareholders will become shareholders of Mylan, which

has a clear track record of creating shareholder value, with an annualized five year total shareholder return of approximately 20.7 percent.4

Certain definitions

Mylan means Mylan N.V., or, depending on the context, the group of which Mylan is the parent company including, following

completion of the Offer, Meda.

Meda means Meda Aktiebolag (publ.), corp. ID No. 556427-2812, or, depending on the context,

the group of which Meda is the parent company.

Combined Company means the combination of Mylan and Meda if the Offer is

completed.

Offer means Mylan’s recommended public offer to the shareholders of Meda in accordance with the terms

specified in this Offer Document.

Offer Document means this offer document.

2016 Bridge Credit Agreement means the bridge credit agreement dated as of February 10, 2016 among Mylan N.V., as borrower, Mylan

Inc., as guarantor, Deutsche Bank AG Cayman Islands Branch, as administrative agent and a lender, Goldman Sachs Bank USA, as a lender, Goldman Sachs Lending Partners LLC, as a lender, and other lenders party thereto from time to time.

Bridge Credit Facility means the bridge credit facility made available to Mylan under the 2016 Bridge Credit Agreement.

Euroclear means Euroclear Sweden AB.

EU Prospectus means the prospectus to be issued in connection with the Offer.

New June 2016 Senior Notes refers to the $6.5 billion aggregate principal amount of Senior Notes, comprised of $1.0 billion

aggregate principal amount of 2.50% Senior Notes due 2019, $2.25 billion aggregate principal amount of 3.15% Senior Notes due 2021, $2.25 billion aggregate principal amount of 3.95% Senior Notes due 2026 and $1.0 billion aggregate principal amount

of 5.25% Senior Notes due 2046, issued by Mylan on June 9, 2016, in a private offering exempt from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”), to qualified institutional buyers in

accordance with Rule 144A and to persons outside of the U.S. pursuant to Regulation S under the Securities Act, as amended.

Nasdaq Stockholm means the Swedish regulated market, Nasdaq Stockholm, or, depending on the context, its market operator Nasdaq

Stockholm Aktiebolag.

Registration Statement means Mylan’s Registration Statement on Form S-4, which has been prepared

in connection with the Offer.

SEC means the U.S. Securities and Exchange Commission.

SEK, EUR/€ and USD/$ mean Swedish kronor, euro and U.S. Dollar, respectively. M means millions.

Transaction means the proposed acquisition of Meda by Mylan pursuant to the Offer.

| 1 |

The Share Cap will be exceeded if the Offeror Average Closing Price is less than USD 30.78, based on 365,467,371 outstanding Meda shares (the number of outstanding Meda shares as of both the date of the announcement of

the Offer and the most recent trading day prior to the date of this Offer Document) and assuming that 100 percent of the outstanding Meda shares will be tendered into the Offer). |

| 2 |

See, e.g., Morgan Stanley Analyst Report, “Mylan Inc.: Updating MYL stand-alone and establishing pro forma Meda deal model,” February 17, 2016.

|

| 3 |

See, e.g., Global Data Industry Report, “Mylan N.V. (MYL) – Financial and Strategic SWOT Analysis Review,” May 2016. |

| 4 |

Total shareholder return data is from Bloomberg and reflects total return (including price appreciation and reinvested dividends) as of December 31, 2015.

|

1

Summary

This summary consists of disclosure requirements known as “Elements,” which are numbered in Sections A – E (A.1 – E.7).

This summary contains all the Elements required to be included in a summary for the type of securities and issuer. Because

some Elements are not required to be addressed, there may be gaps in the numbering sequence of the Elements.

Even though an Element may be required to be inserted in the summary because of the type of securities and issuer, it is

possible that no relevant information can be given regarding the Element. In this case a short description of the Element is included in the summary with the mention of “not applicable.”

|

|

|

|

|

| |

| Section A – Introduction and

warnings |

| A.1 |

|

Introduction and warnings |

|

This summary should be read as an introduction to this Offer Document. |

| |

|

|

Any decision to invest in the Mylan Shares being offered as part of

the Offer should be based on consideration of this Offer Document as a whole by the investor. |

| |

|

|

|

Where a claim relating to the information in this Offer Document is

brought before a court in a Member State of the European Economic Area, the plaintiff investor might, under the national legislation of that Member State, have to bear the costs of translating this Offer Document before the legal proceedings are

initiated. |

| |

|

|

|

Civil liability in relation to this summary may attach to Mylan,

including any translation thereof, but only if the summary is misleading, inaccurate or inconsistent with other parts of this Offer Document or if it does not provide, when read together with other parts of this Offer Document, key information in

order to aid investors when considering whether to invest in the Mylan Shares. |

| A.2 |

|

Consent to the use of this Offer Document for resale or final placement of securities |

|

Not applicable. The Offer is not being marketed by any financial intermediary. |

|

|

|

|

|

| |

| Section B – Issuer |

| B.1 |

|

Legal and commercial name |

|

Mylan’s legal and commercial name is Mylan N.V. The registration number of Mylan N.V. with the Dutch Trade register is 61036137. |

| B.2 |

|

Domicile and legal form |

|

Mylan is a public limited liability company (naamloze vennootschap) organized and existing under the laws of the Netherlands, with its

corporate seat (statutaire zetel) in Amsterdam, the Netherlands, its principal executive offices located at Building 4, Trident Place, Mosquito Way, Hatfield, Hertfordshire, AL10 9UL England and Mylan N.V. group’s global headquarters

located at 1000 Mylan Blvd., Canonsburg, PA 15317 U.S.A. |

| B.3 |

|

Nature of operations and principal activities |

|

Mylan is a leading global pharmaceutical company, which develops, licenses, manufactures, markets and distributes generic, branded generic and

specialty pharmaceuticals.5 Mylan is committed to setting new standards in healthcare by creating better health for a better world, and Mylan’s mission is to provide the world’s 7

billion people access to high quality medicine. To do so, Mylan innovates to satisfy unmet needs; makes reliability and service excellence a habit; does what’s right, not what’s easy; and impacts the future through passionate global

leadership. |

| |

|

|

|

Mylan offers one of the industry’s broadest product portfolios,

including more than 1,400 marketed products, to customers in approximately 165 countries and territories. Mylan operates a global, high quality vertically-integrated manufacturing platform, which includes more than 50 manufacturing

and research and development (“R&D”) facilities around the world and one of the world’s largest active pharmaceutical ingredient (“API”) operations.6

Mylan also operates a strong and innovative R&D |

| |

|

|

|

5 See, e.g., Global Data Industry Report,

“Mylan N.V. (MYL)–Financial and Strategic SWOT Analysis Review,” May 2016. |

| |

|

|

|

6 See, e.g., Global Data Industry Report, “Mylan N.V. (MYL)–Financial and Strategic SWOT Analysis Review,” May

2016. |

2

Summary

|

|

|

|

|

| B.3 |

|

Nature of operations and principal activities, continued |

|

network that has consistently delivered a robust product pipeline including a variety of dosage forms, therapeutic categories and

biosimilars. Additionally, Mylan has a specialty pharmaceutical business that is focused on respiratory and allergy therapies. |

| |

|

|

|

Mylan operates in two segments, “Generics” and

“Specialty.” Mylan’s Generics segment primarily develops, manufactures, sells and distributes generic or branded generic pharmaceutical products in tablet, capsule, injectable, transdermal patch, gel, cream or ointment form, as well

as API. The Specialty segment engages mainly in the development and sale of branded specialty nebulized and injectable products. Mylan’s generic pharmaceutical business is conducted primarily in the U.S. and Canada (collectively, “North

America”); Europe; and India, Australia, Japan, New Zealand and Brazil as well as its export activity into emerging markets (collectively, “Rest of World”). Mylan’s API business is conducted through Mylan Laboratories

Limited, which is included within Rest of World in its Generics segment. Mylan’s specialty pharmaceutical business is conducted by Mylan Specialty L.P. |

| B.4a |

|

Recent trends |

|

The following general trends are applicable to Mylan. In the

U.S., increased sales volumes in the generic pharmaceutical industry are due to, among other factors, Part D of the Medicare Modernization Act, under which Medicare beneficiaries are eligible to obtain prescription drug coverage from private sector

providers, which may be offset by increased pricing pressures due to the enhanced purchasing power of the private sector providers that are negotiating on behalf of Medicare beneficiaries. Mylan also believes that federal or state governments will

continue to enact measures aimed at reducing the cost of drugs to the public under Medicaid, a U.S. federal healthcare program. The U.S. pharmaceutical market is also undergoing, and will likely continue to undergo, rapid and significant

technological changes that are expected to intensify competition. In Europe, legislative changes are expected to move all regions in Spain to INN prescribing and substitution, making pharmacists the key driver of generic usage. Under the tender

system in the Netherlands and Germany, health insurers are entitled to issue invitations to tender products. Pricing pressures resulting from an effort to win the tender should drive near-term competition. In Italy, extended patent protection has

resulted in slower growth in its generics market as compared to other European countries. Government initiatives to lower pricing for pharmaceutical products throughout Europe have in some cases offset Mylan’s increased sales volumes and

penetration in certain growing European markets. In India, Mylan expects exports of API and generic finished dosage form (“FDF”) products will continue to increase, offset in part by increased pressure on prices driven by the

intense competition in the API supply market in recent years, while in Japan, pro-generic government initiatives are expected to lead to growth in the generics market. Similarly, in Brazil, the emergence of generic drug laws has advanced growth in

the generics segment of the pharmaceutical market. |

| |

|

|

|

For the three months ended March 31, 2016, Mylan reported total

revenues of $2.19 billion, compared to $1.87 billion for the comparable prior year period. Mylan’s revenues for the three months ended March 31, 2016 were unfavorably impacted by the effect of foreign currency translation, primarily

reflecting changes in the U.S. Dollar as compared to the currencies of Mylan’s subsidiaries in Europe, India and Australia. The unfavorable impact of foreign currency translation on total revenues for the three months ended March 31, 2016 was

approximately $33 million, or 2 percent. As such, constant currency total revenues increased approximately $352 million, or 19 percent. The increase in constant currency total revenues was the result of constant currency third party

net sales growth in Generics of 19 percent, and Specialty of 17 percent. The impact in the first quarter of 2016 from the additional two months of net sales from the non-U.S. developed markets specialty and branded generics business (the

“EPD Business”) acquired from Abbott Laboratories (“Abbott”) (“incremental EPD Business sales”) compared to the first quarter of 2015, and to a lesser extent, other acquisitions and net sales from

products launched since April 1, 2015 (“new products”), totaled approximately $414.8 million. On a constant currency basis, net sales from existing products decreased approximately $60 million as a result of a decrease in

pricing of approximately $62 million, partially offset by an increase in volume of approximately $2 million. |

| |

|

|

|

Cost of sales for the three months

ended March 31, 2016 was $1.28 billion, compared to $1.04 billion for the comparable prior year period. Cost of sales for the three months ended March 31, 2016 was impacted by purchase accounting related amortization of acquired

intangible assets of approximately $243.6 million, acquisition related costs of approximately $18.5 million and restructuring and other special items of approximately $15.2 million. The prior year comparable period cost of sales included

similar purchase accounting related amortization of approximately $140.2 million, acquisition related costs of approximately $12.3 million and restructuring and other special items of approximately $8.0 million. Gross profit for the three

months ended March 31, 2016 was $907.0 million, and gross margins were 41.4 percent. For the three months ended March 31, 2015, gross profit was $830.1 million, and gross margins were 44.4 percent. Excluding purchase accounting

related amortization, acquisition related costs and restructuring and other special items, adjusted gross margins were approximately 54 percent for the three months ended March 31, 2016, as compared to approximately 53 percent for the

three months ended March 31, 2015. |

3

Summary

|

|

|

|

|

| B.4a |

|

Recent trends, continued |

|

From time to time, a limited number of

Mylan’s products may represent a significant portion of its net sales, gross profit and net earnings. Generally, this is due to the timing of new product launches and the amount, if any, of additional competition in the market. Mylan’s top

ten products in terms of sales, in the aggregate, represented approximately 26 percent and 27 percent of Mylan’s total revenues for the three months ended March 31, 2016 and 2015, respectively. |

| |

|

|

|

For the three months ended March 31, 2016, Generics third party net

sales were $1.93 billion, compared to $1.64 billion for the comparable prior year period, an increase of $284.7 million, or 17.3 percent. In the Generics segment, the unfavorable impact of foreign currency translation on third party net sales

for the three months ended March 31, 2016 was approximately $33 million, or 2 percent. As such, constant currency third party net sales increased by approximately $317 million, or 19 percent when compared to the prior year period. Third party

net sales from North America were $919.7 million for the three months ended March 31, 2016, compared to $855.0 million for the comparable prior year period, representing an increase of $64.7 million, or 7.6 percent. The increase in current

quarter third party net sales was principally due to net sales from new products, and to a lesser extent, the incremental EPD Business sales, totaling approximately $135 million, offset by lower pricing and volumes on existing products.

Third party net sales from Europe were $587.7 million for the three months ended March 31, 2016, compared to $406.2 million for the comparable prior year period, an increase of $181.5 million, or 44.7 percent. This increase was

primarily the result of the incremental EPD Business sales, and to a lesser extent, net sales from new products, totaling approximately $191 million in the first quarter of 2016. Higher volumes on existing products, primarily in France, were offset

by lower pricing throughout Europe as a result of government-imposed pricing reductions and competitive market conditions. In Rest of World, third party net sales were $420.8 million for the three months ended March 31, 2016, compared to $382.3

million for the comparable prior year period, an increase of $38.5 million, or 10.1 percent. This increase was primarily driven by the impact of the incremental EPD Business sales and sales by the female healthcare businesses acquired from

Famy Care Limited (such businesses “Jai Pharma Limited”), and to a lesser extent, new product launches across the region, totaling $89 million, as well as higher volumes in Japan and Australia. These increases were partially offset

by lower pricing throughout the region and a decrease in third party net sales volumes from Mylan’s operations in India, in particular, the anti-retroviral (“ARV”) franchise. |

| |

|

|

|

For the three months ended March 31, 2016, Specialty reported third

party net sales of $247.9 million, an increase of $36.8 million, or 17.4 percent, from $211.1 million for the comparable prior year period. The increase was primarily the result of higher volumes of the EpiPen® Auto-Injector, which is used in the treatment of severe allergic reactions (anaphylaxis), and higher sales of the Perforomist® Inhalation

Solution. |

| |

|

|

|

Mylan’s operating expenses primarily consist of R&D expenses,

selling, general and administrative expense (“SG&A”) and litigation settlements. R&D expense for the three months ended March 31, 2016 was $253.6 million, compared to $169.9 million for the comparable prior year period,

an increase of $83.7 million. In the first quarter of 2016, Mylan made an upfront payment to Momenta for $45 million related to the collaboration agreement entered into on January 8, 2016. R&D expense also increased due to the impact of the

EPD Business. In addition, R&D increased due to the continued development of Mylan’s respiratory, insulin and biologics programs as well as the timing of internal and external product development projects. SG&A for the three months

ended March 31, 2016 was $549.3 million, compared to $483.2 million for the comparable prior year period, an increase of $66.1 million. The increase in SG&A is primarily due to the additional two months of expense related to the EPD

Business, which increased SG&A by approximately $67 million. During the three months ended March 31, 2016 and 2015, Mylan recorded a $1.5 million gain, net, and a $17.7 million charge, net, respectively, in the prior year period for

litigation settlements. In the three months ended March 31, 2016, the gain was primarily related to the settlement of an intellectual property matter. In the prior year period, the charge was primarily related to the settlement of an antitrust

matter. |

| |

|

|

|

The financial information above was derived from Mylan’s

Quarterly Report on Form 10-Q for the three months ended March 31, 2016 and is unaudited. |

| B.5 |

|

Group |

|

Mylan is the parent company of the Mylan group. Mylan has 170 subsidiaries in 43 countries as of December 31,

2015. Mylan’s financial results are reported on a consolidated basis with those of its subsidiaries. |

4

Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| B.6 |

|

Major shareholders, etc. |

|

|

|

The following table lists the names of shareholders known to Mylan to beneficially own more than five percent of the outstanding Mylan Shares as of June 9, 2016 (based on 508,364,554

Mylan Shares issued and outstanding as of such date): |

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|

Name of beneficial owners |

|

Number of shares

beneficially owned |

|

|

Percentage of shares and

votes beneficially owned |

|

|

|

| |

|

|

|

|

|

Subsidiaries of Abbott Laboratories(1) |

|

|

69,750,000(2) |

|

|

|

13.7% |

|

|

|

| |

|

|

|

|

|

Wellington Management Company LLP and affiliates |

|

|

44,793,344(3) |

|

|

|

8.8% |

|

|

|

| |

|

|

|

|

|

BlackRock, Inc. |

|

|

33,735,289(4) |

|

|

|

6.6% |

|

|

|

| |

|

|

|

|

|

(1) Abbott and its

subsidiaries that own Mylan Shares are subject to the terms of the shareholder agreement (the “Abbott Shareholder Agreement”), dated February 27, 2015, by and among Mylan, Abbott, Laboratoires Fournier S.A.S. (“Abbott

France”), Abbott Established Products Holdings (Gibraltar) Limited (“Abbott Gibraltar”), and Abbott Investments Luxembourg S.à.r.l. (“Abbott Luxembourg” and, together with Abbott France and Abbott

Gibraltar, the “Abbott Subsidiaries”). According to Item 4 of the Schedule 13D/A filed by Abbott on August 10, 2015, Abbott Gibraltar distributed 62,782,018 Mylan Shares to Abbott Products (“Abbott Products”), on

July 28, 2015 (the “Distribution”). Contemporaneously with the Distribution, Abbott Products became a party to the Abbott Shareholder Agreement by executing a joinder agreement thereto. As a result of the Distribution, Abbott

Gibraltar no longer beneficially owns any Mylan Shares. The Abbott Shareholder Agreement will terminate when Abbott no longer beneficially owns any of the Mylan Shares issued to it in connection with Mylan’s acquisition of the EPD Business

(together with Mylan’s acquisition of Mylan Inc., the “EPD Transaction”). So long as Abbott beneficially owns at least five percent of the Mylan Shares, Abbott is required to vote each Mylan voting security (a) in favor of all

those persons nominated and recommended to serve as directors of Mylan’s board of directors (the “Mylan Board”) or any applicable committee thereof and (b) with respect to any other action, proposal, or matter to be voted

on by the shareholders of Mylan (including through action by written consent), in accordance with the recommendation of the Mylan Board or any applicable committee thereof. However, Abbott is free to vote at its discretion in connection with any

proposal submitted for a vote of the Mylan shareholders in respect of (a) the issuance of equity securities in connection with any merger, consolidation, or business combination of Mylan, (b) any merger, consolidation, or business combination of

Mylan, or (c) the sale of all or substantially all the assets of Mylan, except where such proposal has not been approved or recommended by the Mylan Board, in which event Abbott must vote against the proposal. |

|

|

|

| |

|

|

|

|

|

(2) Based on Schedule

13D/A filed by Abbott, Abbott Luxembourg and Abbott Products with the SEC on August 10, 2015, Abbott has sole voting power over 0 shares, shared voting power over 69,750,000 shares, sole dispositive power over 0 shares, and shared dispositive

power over 69,750,000 shares; Abbott France has sole voting power, shared voting power, sole dispositive power and shared dispositive power over 0 shares; Abbott Luxembourg has sole voting power over 0 shares, shared voting power over

6,967,982 shares, sole dispositive power over 0 shares, and shared dispositive power over 6,967,982 shares; and Abbott Products has sole voting power over 0 shares, shared voting power over 62,782,018 shares, sole dispositive power over 0

shares, and shared dispositive power over 62,782,018 shares. |

|

|

|

| |

|

|

|

|

|

(3) Based on Schedule 13G/A

filed by Wellington Management Group LLP, Wellington Group Holdings LLP, Wellington Investment Advisors Holdings LLP and Wellington Management Company LLP with the SEC on February 11, 2016, Wellington Management Group LLP has sole voting power over

0 shares, shared voting power over 13,546,750 shares, sole dispositive power over 0 shares, and shared dispositive power over 44,793,344 shares; Wellington Group Holdings LLP has sole voting power over 0 shares, shared voting power over

13,546,750 shares, sole dispositive power over 0 shares, and shared dispositive power over 44,793,344 shares; Wellington Investment Advisors Holdings LLP has sole voting power over 0 shares, shared voting power over 13,546,750 shares, sole

dispositive power over 0 shares, and shared dispositive power over 44,793,344 shares; and Wellington Management Company LLP has sole voting power over 0 shares, shared voting power over 12,489,471 shares, sole dispositive power over 0 shares,

and shared dispositive power over 42,867,413 shares. Based on the Schedule 13G/A, the securities as to which the Schedule 13G/A was filed are owned of record by clients of one or more investment advisers identified therein directly or indirectly

owned by Wellington Management Group LLP. Those clients have the right to receive, or the power to direct the receipt of, dividends from, or the proceeds from the sale of, such securities. No such client is known to have such right or power with

respect to more than five percent of this class of securities. |

|

|

|

| |

|

|

|

|

|

(4) Based on Schedule 13G

filed by BlackRock, Inc. with the SEC on February 9, 2016, BlackRock, Inc. has sole voting power over 30,656,253 shares, shared voting power over 0 shares, sole dispositive power over 33,735,289 shares, and shared dispositive power over 0

shares. |

|

|

|

| |

|

|

|

|

|

All shares in Mylan’s capital carry one vote, so all shareholders have a number of voting rights equal to the number of shares that they hold. |

|

|

|

| B.7 |

|

Selected historical financial information |

|

|

|

The following table sets forth the selected historical financial information of Mylan as of and for each of the years in the three-year period ended December 31, 2015 and as of and

for the three months ended March 31, 2016 and 2015. The selected historical financial information as of and for the years ended December 31, 2015, 2014 and 2013 has been derived from Mylan’s audited consolidated financial statements. The

unaudited selected historicial financial information as of and for the three months ended March 31, 2016 and 2015 has been derived from Mylan’s unaudited condensed consolidated financial statements which include, in the opinion of

Mylan’s management, all normal and recurring adjustments that are necessary for the fair presentation of the results for such interim periods and dates. The historical consolidated financial statements of Mylan are prepared in accordance with

U.S. GAAP. Mylan N.V. is considered the successor to Mylan Inc., and the information set forth below refers to Mylan Inc. for periods prior to February 27, 2015, and to Mylan N.V. on and after February 27, 2015. On February 27, 2015, Mylan

completed the acquisition of the EPD Business. The results of the EPD Business’s operations have been included in Mylan’s consolidated financial statements since the acquisition date. The selected historical financial information may not

be indicative of the future performance of Mylan. |

|

|

|

| |

|

|

|

|

|

There has been no material change in the Mylan group’s financial or

trading position since March 31, 2016. |

|

|

|

5

Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

| B.7 |

|

Selected historical

financial information,

continued |

|

|

|

(Unaudited)

Three Months Ended

March 31, |

|

|

Year Ended December 31, |

|

| |

|

|

|

(USD, in millions, except per share

amounts) |

|

2016 |

|

|

2015 |

|

|

2015 |

|

|

2014 |

|

|

2013 |

|

| |

|

|

|

| |

|

|

|

Selected Statements of Operations Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Total revenues |

|

|

$2,191.3 |

|

|

|

$1,871.7 |

|

|

|

$9,429.3 |

|

|

|

$7,719.6 |

|

|

|

$6,909.1 |

|

| |

|

|

|

Cost of sales |

|

|

1,284.3 |

|

|

|

1,041.6 |

|

|

|

5,213.2 |

|

|

|

4,191.6 |

|

|

|

3,868.8 |

|

| |

|

|

|

|

|

| |

|

|

|

Gross profit |

|

|

907.0 |

|

|

|

830.1 |

|

|

|

4,216.1 |

|

|

|

3,528.0 |

|

|

|

3,040.3 |

|

| |

|

|

|

Operating expenses |

|

|

801.4 |

|

|

|

670.8 |

|

|

|

2,755.2 |

|

|

|

2,175.4 |

|

|

|

1,904.8 |

|

| |

|

|

|

|

|

| |

|

|

|

Earnings from operations |

|

|

105.6 |

|

|

|

159.3 |

|

|

|

1,460.9 |

|

|

|

1,352.6 |

|

|

|

1,135.5 |

|

| |

|

|

|

Interest expense |

|

|

70.3 |

|

|

|

79.5 |

|

|

|

339.4 |

|

|

|

333.2 |

|

|

|

313.3 |

|

| |

|

|

|

Other expense (income), net |

|

|

16.3 |

|

|

|

18.5 |

|

|

|

206.1 |

|

|

|

44.9 |

|

|

|

74.9 |

|

| |

|

|

|

|

|

| |

|

|

|

Earnings before income taxes and noncontrolling interest |

|

|

19.0 |

|

|

|

61.3 |

|

|

|

915.4 |

|

|

|

974.5 |

|

|

|

747.3 |

|

| |

|

|

|

Income tax provision |

|

|

5.1 |

|

|

|

4.7 |

|

|

|

67.7 |

|

|

|

41.4 |

|

|

|

120.8 |

|

| |

|

|

|

Net earnings attributable to the noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

(0.1) |

|

|

|

(3.7) |

|

|

|

(2.8) |

|

| |

|

|

|

|

|

| |

|

|

|

Net earnings attributable to Mylan N.V. ordinary shareholders |

|

|

$13.9 |

|

|

|

$56.6 |

|

|

|

$847.6 |

|

|

|

$929.4 |

|

|

|

$623.7 |

|

| |

|

|

|

|

|

| |

|

|

|

Earnings per ordinary share attributable to Mylan N.V. ordinary shareholders: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Basic |

|

|

$0.03 |

|

|

|

$0.14 |

|

|

|

$1.80 |

|

|

|

$2.49 |

|

|

|

$1.63 |

|

| |

|

|

|

Diluted |

|

|

$0.03 |

|

|

|

$0.13 |

|

|

|

$1.70 |

|

|

|

$2.34 |

|

|

|

$1.58 |

|

| |

|

|

|

Weighted average ordinary shares outstanding: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Basic |

|

|

489.8 |

|

|

|

418.0 |

|

|

|

472.2 |

|

|

|

373.7 |

|

|

|

383.3 |

|

| |

|

|

|

Diluted |

|

|

509.6 |

|

|

|

443.8 |

|

|

|

497.4 |

|

|

|

398.0 |

|

|

|

394.5 |

|

| |

|

|

|

|

|

| |

|

|

| |

|

|

|

(USD, in millions) |

|

| |

|

|

|

Selected Balance Sheet data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Total current assets |

|

|

$6,627.6 |

|

|

|

$7,426.4 |

|

|

|

$6,472.7 |

|

|

|

$6,441.2 |

|

|

|

$4,471.2 |

|

| |

|

|

|

Total assets |

|

|

22,644.1 |

|

|

|

22,123.8 |

|

|

|

22,267.7 |

|

|

|

15,820.5 |

|

|

|

15,294.8 |

|

| |

|

|

|

Total current liabilities |

|

|

3,959.4 |

|

|

|

5,228.0 |

|

|

|

4,122.2 |

|

|

|

5,304.0 |

|

|

|

2,964.0 |

|

| |

|

|

|

Total equity |

|

|

10,274.9 |

|

|

|

9,093.2 |

|

|

|

9,765.8 |

|

|

|

3,276.0 |

|

|

|

2,959.9 |

|

| |

|

|

|

Total liabilities and equity |

|

|

$22,644.1 |

|

|

|

$22,123.8 |

|

|

|

$22,267.7 |

|

|

|

$15,820.5 |

|

|

|

$15,294.8 |

|

| |

|

|

| |

|

|

|

(USD, in millions) |

|

| |

|

|

|

Selected Cash Flow data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Net cash provided by operating activities |

|

|

$80.5 |

|

|

|

$267.0 |

|

|

|

$2,008.5 |

|

|

|

$1,014.8 |

|

|

|

$1,106.6 |

|

| |

|

|

|

Net cash used in investing activities |

|

|

(160.0) |

|

|

|

(87.5) |

|

|

|

(1,569.7) |

|

|

|

(800.3) |

|

|

|

(1,868.8) |

|

| |

|

|

|

Net cash provided by (used in) financing activities |

|

|

30.5 |

|

|

|

(109.0) |

|

|

|

604.8 |

|

|

|

(267.4) |

|

|

|

692.9 |

|

| |

|

|

|

Effect on cash of changes in exchange rates |

|

|

12.4 |

|

|

|

(18.8) |

|

|

|

(33.1) |

|

|

|

(12.9) |

|

|

|

10.6 |

|

| |

|

|

|

|

|

| |

|

|

|

Net (decrease) increase in cash and cash equivalents |

|

|

(36.6) |

|

|

|

51.7 |

|

|

|

1,010.5 |

|

|

|

(65.8) |

|

|

|

(58.7) |

|

| |

|

|

|

Cash and cash equivalents – beginning of period |

|

|

1,236.0 |

|

|

|

225.5 |

|

|

|

225.5 |

|

|

|

291.3 |

|

|

|

350.0 |

|

| |

|

|

|

|

|

| |

|

|

|

Cash and cash equivalents – end of period |

|

|

$1,199.4 |

|

|

|

$277.2 |

|

|

|

$1,236.0 |

|

|

|

$225.5 |

|

|

|

$291.3 |

|

| |

|

|

|

|

|

| |

|

|

| |

|

|

|

(USD, in millions) |

|

| |

|

|

|

Selected Comprehensive Earnings data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Net earnings attributable to Mylan N.V. ordinary shareholders |

|

|

$13.9 |

|

|

|

$56.6 |

|

|

|

$847.7 |

|

|

|

$933.1 |

|

|

|

$626.5 |

|

| |

|

|

|

Other comprehensive earnings (loss), net of tax |

|

|

473.8 |

|

|

|

(623.9) |

|

|

|

(777.3) |

|

|

|

(746.9) |

|

|

|

(153.6) |

|

| |

|

|

|

Comprehensive earnings attributable to the noncontrolling interest |

|

|

– |

|

|

|

– |

|

|

|

(0.1) |

|

|

|

(3.7) |

|

|

|

(2.8) |

|

| |

|

|

|

|

|

| |

|

|

|

Comprehensive earnings (loss) attributable to Mylan N.V. ordinary shareholders |

|

|

$487.7 |

|

|

|

$(567.3) |

|

|

|

$70.3 |

|

|

|

$182.5 |

|

|

|

$470.1 |

|

| |

|

|

|

|

|

| |

|

|

|

|

| |

|

|

|

|

|

Three Months Ended

March 31, |

|

|

Year Ended December 31, |

|

| |

|

|

|

Key Ratios |

|

2016 |

|

|

2015 |

|

|

2015 |

|

|

2014 |

|

|

2013 |

|

| |

|

|

|

|

|

| |

|

|

|

Gross margin |

|

|

41.4% |

|

|

|

44.4% |

|

|

|

44.7% |

|

|

|

45.7% |

|

|

|

44.0% |

|

| |

|

|

|

Operating margin |

|

|

4.8% |

|

|

|

8.5% |

|

|

|

15.5% |

|

|

|

17.5% |

|

|

|

16.4% |

|

6

Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| B.8 |

|

Selected unaudited pro forma financial information |

|

The following selected unaudited pro forma financial information gives effect to the acquisition of the EPD Business and the proposed acquisition of Meda pursuant to the Offer, both

of which are accounted for under the acquisition method of accounting in accordance with the Financial Accounting Standards Board’s Accounting Standards Codification (“ASC”) 805, Business Combinations, with Mylan as the

acquirer. The consolidated financial statements of Mylan and the EPD Business are prepared in accordance with U.S. GAAP with all amounts stated in U.S. Dollars. The consolidated financial statements of Meda are prepared in accordance with IFRS and

interpretations issued by the IFRS Interpretations Committee (“IFRS IC”) as adopted by the European Union (the “EU”), the Swedish Annual Accounts Act and the Swedish Financial Reporting Board’s recommendation

RFR 1 Supplementary Accounting Rules for Groups, with all amounts presented in Swedish kronor. The selected unaudited pro forma financial information has been prepared in accordance with U.S. GAAP. The selected unaudited pro forma condensed combined

balance sheet as of March 31, 2016 is based on the unaudited condensed consolidated balance sheet of Mylan as of March 31, 2016 and the unaudited consolidated balance sheet of Meda as of March 31, 2016, converted to U.S. GAAP and U.S. Dollars and

conformed to Mylan’s presentation, and has been prepared to reflect the proposed acquisition of Meda as if it had occurred on March 31, 2016. The selected unaudited pro forma condensed combined statements of operations for the three months

ended March 31, 2016 and the year ended December 31, 2015 are based on the unaudited condensed consolidated statement of operations of Mylan for the three months ended March 31, 2016, the audited consolidated statement of operations of Mylan for the

year ended December 31, 2015, the unaudited consolidated income statement of Meda for the three months ended March 31, 2016, the audited consolidated income statement of Meda for the year ended December 31, 2015, with each such consolidated

income statement of Meda converted to U.S. GAAP and U.S. Dollars and conformed to Mylan’s presentation, and the unaudited EPD Business combined results of operations for the period from January 1, 2015 to February 27, 2015, the acquisition date

of the EPD Business, and has been prepared to reflect the acquisition of the EPD Business and the proposed acquisition of Meda as if each had occurred on January 1, 2015. The selected unaudited pro forma financial information reflects only pro forma

adjustments that are factually supportable and directly attributable to the acquisition of the EPD Business and the proposed acquisition of Meda and, with respect to the selected unaudited pro forma condensed combined statement of operations,

expected to have a continuing impact on the results of the Combined Company. |

|

| |

|

|

|

The selected unaudited pro forma financial information has been derived from the more detailed unaudited pro forma

financial information appearing elsewhere in this Offer Document and the related notes thereto. |

|

| |

|

|

|

The selected unaudited pro forma financial information is for illustrative purposes only. It does not purport to

indicate the results that would have actually been attained had the acquisition of the EPD Business and the proposed acquisition of Meda been completed on the assumed dates or for the periods presented, or which may be realized in the future. To

produce the unaudited pro forma financial information, Mylan allocated the estimated purchase price for Meda using its best estimates of fair value. Such estimates are preliminary and subject to further adjustments, which could be material. To the

extent there are significant changes to the Meda business, the assumptions and estimates herein could change significantly. Due to its nature, the selected unaudited pro forma financial information addresses a hypothetical situation and does not

therefore represent Mylan or the Combined Company’s actual financial position or results. |

|

| |

|

|

|

The selected unaudited pro forma financial information has been prepared assuming that 100 percent of the

outstanding Meda shares will be tendered into the Offer. |

|

| |

|

|

| |

|

|

|

Selected Unaudited Pro Forma Condensed Combined Balance Sheet Information |

|

| |

|

|

|

| |

|

|

|

|

|

March 31, 2016 |

|

| |

|

|

|

(USD, in millions) |

|

Mylan |

|

|

Meda |

|

|

Pro forma

adjustments |

|

|

Pro forma

combined |

|

| |

|

|

|

Total assets |

|

|

$22,644.1 |

|

|

|

$7,312.2 |

|

|

|

$ 6,212.8 |

|

|

|

$36,169.1 |

|

| |

|

|

|

Long-term debt, including current portion |

|

|

7,408.2 |

|

|

|

2,757.2 |

|

|

|

6,429.9 |

|

|

|

16,593.3 |

|

| |

|

|

|

Total liabilities |

|

|

12,369.2 |

|

|

|

4,716.8 |

|

|

|

7,631.9 |

|

|

|

24,717.9 |

|

| |

|

|

|

Total equity |

|

|

10,274.9 |

|

|

|

2,595.4 |

|

|

|

(1,419.1) |

|

|

|

11,451.2 |

|

7

Summary

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

| B.8 |

|

Selected unaudited pro forma financial information, continued |

|

Selected Unaudited Pro Forma Condensed Combined Statements of Operations Information |

|

| |

|

|

|

| |

|

|

|

|

|

|

Three Months Ended March 31, 2016 |

|

| |

|

|

|

(USD, in millions, except per share amounts) |

|

|

Mylan |

|

|

Meda |

|

|

Pro forma

adjustments |

|

|

Pro forma

combined |

|

| |

|

|

|

Total revenues |

|

|

|

$2,191.3 |

|

|

|

$510.7 |

|

|

|

$ (14.3 |

) |

|

|

$2,687.7 |

|

| |

|

|

|

Cost of sales |

|

|

|

1,284.3 |

|

|

|

279.2 |

|

|

|

5.4 |

|

|

|

1,568.9 |

|

| |

|

|

|

Gross profit |

|

|

|

907.0 |

|

|

|

231.5 |

|

|

|

(19.7) |

|

|

|

1,118.8 |

|

| |

|

|

|

Operating expenses |

|

|

|

801.4 |

|

|

|

191.7 |

|

|

|

(24.3) |

|

|

|

968.8 |

|

| |

|

|

|

Other expense, net |

|

|

|

86.6 |

|

|

|

28.0 |

|

|

|

(54.1) |

|

|

|

168.7 |

|

| |

|

|

|

Earnings before income taxes and noncontrolling interest |

|

|

|

19.0 |

|

|

|

11.8 |

|

|

|

(49.5) |

|

|

|

(18.7) |

|

| |

|

|

|

Income tax (benefit) provision |

|

|

|

5.1 |

|

|

|

(21.9) |

|

|

|

(9.9) |

|

|

|

(26.7) |

|

| |

|

|

|

Net earnings attributable to Mylan N.V. ordinary shareholders |

|

|

|

13.9 |

|

|

|

33.7 |

|

|

|

(39.6) |

|

|

|

8.0 |

|

| |

|

|

|

Earnings per ordinary share attributable to Mylan N.V. ordinary shareholders: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

Basic |

|

|

|

$0.03 |

|

|

|

$0.09 |

|

|

|

|

|

|

|

$0.02 |

|

| |

|

|

|

Diluted |

|

|

|

$0.03 |

|

|

|

$0.09 |

|

|

|

|

|

|

|

$0.01 |

|

| |

|

|

|

|

|

| |

|

|

|

| |

|

|

|